VCs and Opportunity Zones

Recently, we had the pleasure of hosting Navin Sethi with Ernst & Young LLP on a webinar to discuss the new Opportunity Zones program created by the recent tax cut law (if you missed it, click here for a recording). Navin frequently counsels wealth and asset management firms on partnership tax matters as well as providing guidance on how Opportunity Zones can apply to venture capital investments.

The goal of the Opportunity Zones program is to drive more investment in underserved areas. Because venture capital investment is critical to economic growth and opportunity, our intent is to explore how compatible Opportunity Zones are to the startup investment model. This post will build off the great content we got from the webinar, provide a brief overview of the program, and go through some frequently asked questions from NVCA membership.

Opportunity Zones Overview

Created as part of the Tax Cuts and Jobs Act, the Opportunity Zones program provides tax incentives for creating dedicated “Opportunity Funds” which will invest in Opportunity Zones. Yes, in order to take advantage of the program, your fund must be dedicated to investing in Opportunity Zones, and we will touch on how that is defined later. Opportunity Zones are economically-distressed census tracts across the country that have been designated for this benefit by state governments, with final sign-off by Treasury. This map shows Opportunity Zones across the country that are now certified.

Potential Benefits for Opportunity Funds

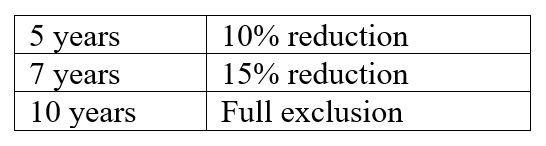

In order for a VC to take advantage of the program, they must first raise a dedicated Opportunity Fund. While other capital can be included in the fund, the tax benefits are only available to capital gains rolled over from existing investments, which have all taxes deferred if invested within 180 days. In addition to this tax deferral, investments by an Opportunity Fund incur the following capital gains reductions based upon hold period of the fund’s investments:

Maintaining Eligibility for Opportunity Funds

Once the capital is raised, a fund can self-certify as an Opportunity Fund. There are semi-annual requirements to check on the eligibility of the fund, and at each review at least 90% of the fund’s assets must be invested in Opportunity Zone assets. Further guidance on how this test will be applied to funds in initial stages should be provided in the coming months by the government.

One of the most significant hurdles for VCs and startups is that at least 50% of the Opportunity Zone business’s gross income must come from inside the zone in which they are based. We will continue to monitor this issue and have a little more discussion on it in the Q&A below, but it’s worth close examination for VCs and could affect interest in the program.

Q&A with Navin

With a little bit of the overview out of the way, let’s get into some venture-specific questions that Navin can answer. These are questions that were either submitted prior to, or during the webinar we hosted for VCs across the country, but which we think are helpful for anybody who may create an Opportunity Fund to consider. For any further questions, please get in touch with Justin Field (jfield@nvca.org) or Navin Sethi (navin.sethi@ey.com).

Q: What event triggers the timeline for deployment of capital into qualifying investments, and how long is this timeframe from the trigger to when at least 90% of the assets have to be invested?

A: Not fully clear yet, but we do know that an investor has 180 days to roll capital gains over into an Opportunity Fund, and then the fund has 180 days to deploy the assets before they will have to meet their 90% test for the first time. It’s important to remember though that the second 180 days could work off the end of year, meaning you’re better off waiting to launch the fund in January rather than November as a November fund launch could have to meet the 90% test the following month! If this continues to be the case, certainly not ideal from a VC perspective, there would likely have to be some advance research and planning before the launch of the fund to avoid failing the first 90% test. It may make sense to get commitments first but wait to pull the investment into the fund until you’re ready to make investments.

Q: What is the 90% test?

A: This is a semi-annual test that an Opportunity Fund must conduct at the mid-point and end of each year, where 90% of the fund’s assets must be in qualifying Opportunity Zone investments at the time of each test.

Q: What is the 50% test?

This test requires that at least 50% of a portfolio company’s gross income must be sourced from inside the Opportunity Zone.

Q: Will the 50% test be an issue for VC investment?

A: It could be depending on how it is applied, but there are some interesting conversations coming out of Treasury where they are talking about how negative gross income that is sourced into Opportunity Zones could be qualifying for purposes of the test. This could mean that losses sourced to the portfolio company count as negative gross income, thus helping a startup meet the test. How that works with no additional guidance we have no idea, but I strongly recommend VCs look further into this if they are interested in launching an Opportunity Fund.

Q: While It’s clear in a VC context that the portfolio companies would have to be in Opportunity Zones, would the funds themselves have to located in one or can they be anywhere?

A: We believe at this point that the funds can be located anywhere, so long as it’s in the U.S. or U.S. possession.

Q: Can Opportunity Funds invest with convertible notes?

A: Having debt won’t be a problem, but it won’t be an eligible interest. You need to have an equity interest to qualify for the tax benefit.

Q: Are all Opportunity Funds going to be closed-end vehicles?

A: Not necessarily, but open-ended funds will have a harder time meeting the 90% test.

Q: Can a fund of funds invest in an Opportunity Zone and pass the tax benefits along to their investors?

A: We believe so at present.

Q: For VCs with investors who will be looking to roll over their gains from their funds, what sort of documentation should they be prepared to provide to ensure a smooth transition?

A: For any significant gains, you should have the gain allocation by partner available even before the K-1 is released. This may require the VC fund to do tax estimates after each investment exit to determine each investors allocation of the eligible gain.

Q: What happens if a startup initially qualifies and receives an investment, but then as it grows, moves out of the zone? Does the initial investment still qualify or is the deferral benefit lost?

A: It’s difficult to say, and there will have to be more work done to clarify. One piece of advice is to have conversations with these startup companies and make sure they are comfortable staying there for a period of time. It will likely be left to further guidance for a clear answer.

Q: What about companies where headquarters are somewhere else, but a branch of the firm is located in an Opportunity Zone? Like say for instance, the management team is in Palo Alto, but the marketing team is in an Opportunity Zone in Oakland?

A: You still have to make sure that you are following the test. If the money goes into the startup, you have to show that it flows to the activity in the zone. So it’s possible, but as above we will need a lot more guidance to understand the mechanics.

Q: If you have a startup that moves into an Opportunity Zone, will further investments in that company qualify?

A: We believe so, particularly if they only have one location of operations and meet the 50% gross income test.

Q: Given the fact that the Opportunity Zone designations expire after 2028, what happens to Opportunity Fund investments after that?

A: The proposed regulations provide that gains from an Opportunity Fund can still realize the tax benefits after expiration so long as that election is made by the end of 2047.

Q: How does the Opportunity Zone program interact with Qualified Small Business Stock (QSBS) rules?

A: It’s likely to be one or the other, but I’m not sure if Treasury has even thought about this yet. If your Opportunity Fund doesn’t work out, you potentially could default to QSBS benefits so long as you adhere to those rules. So advice here is even if you are full steam ahead on Opportunity Zones, be sure to not ignore doing the work to ensure QSBS eligibility.