Timely Reauthorization of PDUFA & MDUFA Is Critical to VC-backed Life Science Breakthroughs

Thirty years ago, the median time for the Food and Drug Administration (FDA) approval of a new drug was 33 months. As one can imagine, major backlog at the agency caused significant delay to the approval and entry of potentially life-saving drugs in the market. To address this problem, Congress passed the Prescription Drug User Fee Act in 1992 to authorize the FDA to collect fees when new drug applications were submitted. Those user fees, paid for by the biopharmaceutical industry, supplemented Congressional funding for the agency to review new drug applications in a more timely and efficient manner. Ten years later, Congress passed the Medical Device User Fee and Modernization Act (MDUFA) after the FDA’s medical device program experienced a substantial loss in resources, seeking to accomplish a shared goal (between industry and the FDA) of improving the review process for new medical devices.

Collectively referred to as the “UFAs”, PDUFA and MDUFA must be reauthorized by Congress every five years. The reauthorization cycle prompts an important collaboration between the FDA and both biopharmaceutical and medical device industries on a number of items, including evaluation of FDA performance, establishing new goals and objectives, and the negotiation of user fees paid for by industry. Congress then receives the proposed user fee agreement from FDA to convene discussion hearings and ultimately to consider reauthorization legislation.

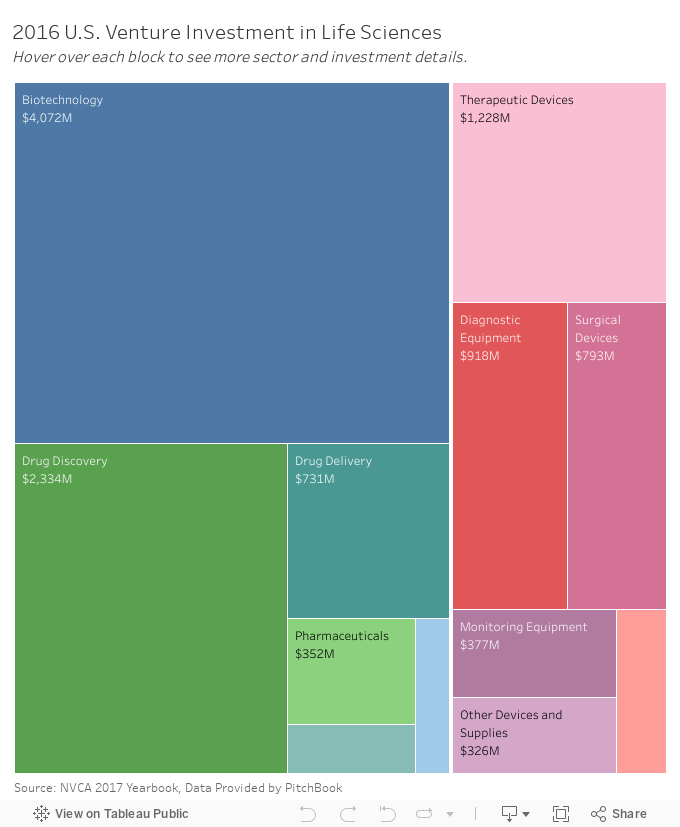

Life science investors are familiar with the FDA approval process for drugs and devices, and understand the need for a capable regulatory body to accelerate the medical innovation occurring within the industry. Venture investment has driven significant growth into many of our country’s most innovative and lifesaving medical products. In fact, the number of life science deals accounted for 12.5% of the overall venture deal count in 2016, investing in some of the most transformative and promising advancements in health care. Last year, $7.79 billion of venture capital was invested in the pharmaceutical and biotechnology sector and $3.86 billion of venture capital was invested in healthcare devices and supplies, representing 17% of overall venture activity. Noteworthy examples of venture-backed life science companies include Moderna, a developer of drugs for genetic disorders, hemophilic and blood factors, and oncology; Human Longevity, a developer of genomics and cell therapy-based diagnostic and therapeutic technology; and CVRx, a developer of implantable technology for the treatment of high blood pressure and heart failure.

It is certainly true that many venture-backed life science startups have seen extraordinary success, but it is important to recognize that medical breakthroughs are extremely challenging and expensive to develop. Those breakthroughs are made even more challenging when there is a lack of certainty on whether FDA will properly staffed and funded. Providing stable funding and resources to meet performance standards at the FDA is absolutely essential for attracting future investment and further expanding our nation’s vibrant medical innovation ecosystem.

Over the next several weeks, Members of the Senate HELP Committee and the House Energy and Commerce Committee will hold hearings to examine these user fee programs, starting first with PDUFA and moving to MDUFA later in the month. The UFAs are set to expire the end of September and we are encouraged that Congress is taking significant action toward reauthorization. At the same time, a packed legislative agenda means that Congress and the Trump Administration will need to prioritize reauthorization of the UFAs to meet the September 30 deadline. We encourage policymakers to work in a collaborative manner to ensure medical innovation continues unimpeded.